Absa commentary on the January 2016 NAAMSA New Vehicle Sales and Exports Report.

Vehicle Sales and Exports

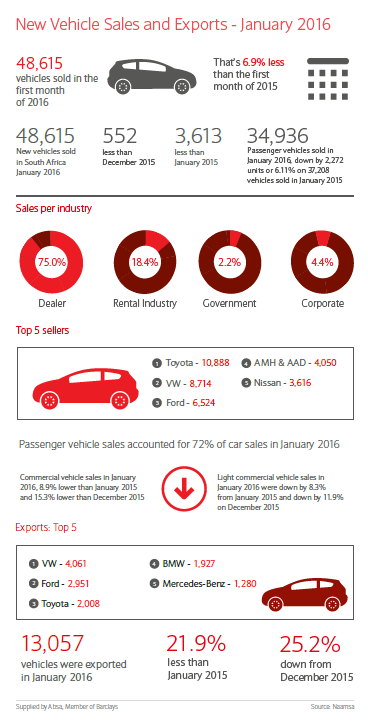

- A total of 48 615 new vehicles were sold in the South African market in January 2016, which were 552 units and 1.1% less than total sales volumes in December last year. Sales were down by 3 613 units in January compared to a year ago, resulting in a decline of 6.9% year-on-year (y/y).

- Of total industry sales of 48 615 units in January, 75% represented dealer sales, 18.4% represented sales to the vehicle rental industry, 4.4% of sales were to corporate fleets and 2.2% represented sales to the government.

- Passenger car sales amounted to 34 936 units (71.9% of total vehicle sales) in January, which were 6.1% less than in January last year, but 5.8% higher than in December. Commercial vehicle sales were down by 8.9% y/y in January, with light commercial vehicles sales (24.8% of total vehicle sales) declining by 8.3% y/y and 11.9% month-on-month (m/m) to a total of 12 074 units.

- The overall daily sales rate came to 2 431 units in January compared with 2 341 units in December.

- New vehicle exports dropped sharply by 21.9% y/y and 25.2% m/m to a total of 13 057 units in January.

Vehicle Finance

- Vehicles are currently mostly financed over a 72-month period with used vehicles only marginally impacting the average financing term. The main driver of this remains affordability, but it has the downside of an ever-increasing average contract period, which continues to lengthen the vehicle replacement cycle.

- The ratio of used to new cars financed was 1.64 at the end of December last year. A total of 25 286 used vehicles were financed in December, with the number of new vehicles financed at 15 465. The total number of vehicles financed in 2015 came to 474 550 (491 569 in 2014), of which 300 101 were used (308 267 used vehicles financed in 2014) and 174 449 were new (183 302 new vehicles financed in 2014), with a used-to-new ratio of 1.72 last year compared with a ratio of 1.68 in 2014.

- Comments and statistics on applications received and electronically scored by Absa in January.

- Absa experienced a decrease in the number of applications received and a decrease in the approval rate.

- Applications received and scored with a 72 month finance term = 90%

- Applications received and scored with balloon payments = 28%

Industry Outlook

- New vehicle sales volumes are forecast to be significantly lower in 2016 compared with the almost 618 000 units sold in 2015. The most important factors that will affect new vehicle sales this year include economic growth, interest rates, household and business financial conditions, and levels of confidence. NAAMSA expects passenger car sales to be down by 9% in 2016, with new commercial vehicles sales forecast to be down by between 3% and 5%.

- Entry-level passenger cars, new model releases and manufacturer incentives will continue to be the main contributors to new vehicle sales volumes for the rest of the year.

- NAAMSA expects new vehicle exports to grow by about 12% to approximately 375 000 units in 2016. Exports will be driven by global economic growth and manufacturers’ export programs. An expected weaker rand exchange rate towards year-end will give further support to vehicle export competitiveness.

- As a result of inflationary pressures, interest rates are forecast to rise further over the next 12-18 months, which will affect the affordability of and the demand for and growth in vehicle finance.

Consumer Outlook

- Consumers are expected to face increased financial strain in 2016 and 2017 on the back of rising inflation and interest rates. Credit-risk profiles are to stay under pressure and will remain a key factor in the accessibility of credit. Access to credit is an important factor in the vehicle market in view of a persistent severe lack of savings.

- Consumers continue to struggle in obtaining and affording credit for higher-priced vehicles, with the demand for favourably priced entry-level vehicles and good-quality used vehicles remaining strong.

Factors Impacting the Vehicle Sector

- Vehicle prices (exchange rate, taxes, input costs): New vehicle price inflation set to remain under upward pressure due to expected further rand weakness in 2016-17.

- Household finances (household income, employment, inflation, ratio of household debt to disposable income and consumer credit-risk profiles), business sector performance and consumer and business confidence: Household finances remain finely balanced with debt levels still high and the percentage of credit-active consumers having impaired credit records remaining on a gradual rising trend. Consumer and business confidence remains low against the background of economic developments.

- Vehicle finance (interest rates, banks’ risk appetite and lending criteria, legislation and regulation): The demand for and affordability and accessibility of vehicle finance, largely driven by interest rate movements, customer credit-risk profiles and consumer and business confidence, will remain important to the performance of vehicle sales.

- Transport costs (fuel prices and maintenance costs): Fuel prices and vehicle maintenance costs drive transport costs and consumer price inflation, impacting consumer and business spending power.

- Economic performance and vehicle demand and supply (global and domestic economic growth, exports and workforce stability): Global and domestic economic growth will drive domestic vehicle sales and exports, which will be supported by manufacturers’ export programs, with labour market trends and developments impacting vehicle production and export volumes. Vehicle export competitiveness will benefit from a depreciating exchange rate.