Social solidarity principles of healthcare insurance leaves younger, healthier members with short end of the stick

One of the many obstacles to South Africa’s private healthcare system functioning like a competitive marketplace are the social solidarity principles which require that all members within a medical scheme contribute equally into a pool of funds whether they are young and healthy, or elderly and sickly. Effectively there is no individual risk-rating as is the case in the short-term insurance sector, like vehicle insurance as one example.

Effectively it means that the young and healthy subsidise the elderly and sickly, and higher claimants who make use of their medical scheme benefits significantly more than their younger counterparts. In this environment, everyone pays the same, regardless of age or benefit usage.

“As a result, younger people and families simply cannot afford the high cost of private healthcare they desperately need and so remain either uninsured, or underinsured and at significant risk given the dire state of South Africa’s public healthcare facilities,” explains Ceazare de Beer, CEO of GapX, a gap insurance provider by GENRIC Insurance company Limited.

“By artificially raising the cost of medical scheme premiums for younger members to subsidise the elderly, many young people are questioning the value proposition of medical scheme benefits. For those who understand the importance of having private healthcare given the parlous state of public health facilities, many are now opting for lower benefit medical scheme options such as core hospital plans to keep things affordable, and then backing this up with a gap insurance product to cover any shortfalls in hospitalisation treatment not covered by their medical scheme.

Gap insurance was specifically formulated to protect medical scheme members from the onerous financial implications which arise from the differences between the rate that specialists charge for in-hospital procedures versus what the medical scheme pays – with gaps of up to 400% becoming the norm,” says Ceazare.

However, until recently, most traditional gap insurance providers have operated on the same social solidarity principles as medical schemes.

“As a new gap cover product, GapX takes a different approach and believes that younger and healthier members should get the financial benefits of their risk ratings, and secondly, should be able to use technology platforms to cut down on administration and further save on costs. Our gap cover is rated according to age, so younger and healthier members and smaller families get a far more favourable rating and premium price, which makes their essential healthcare covers more affordable.

The reality is that cross-subsidisation unfairly drives up the price of medical gap cover, putting more pressure on younger medical aid members trying to protect themselves from rising healthcare costs. We want to change this by removing cross-subsidisation from young to old,” explains Ceazare.

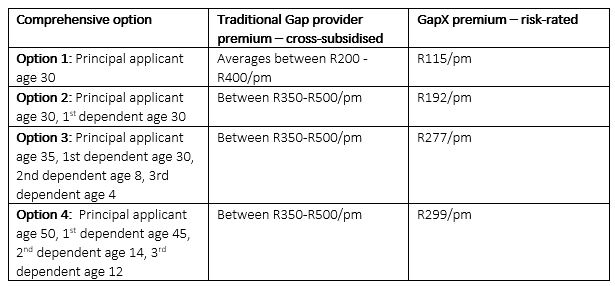

GapX premiums are determined by the age of each person insured and the size of the family covered. Traditionally there has been a one-size-fits-all approach to premiums by grouping together policyholders in broad groups for individuals, families and pensioners. This impacts young individuals and families the most who have to pay more than their fair share in order to subsidise older individuals and larger families, yet they use their benefits the least.

The following example illustrates the impact that cross-subsidising has on Gap premium costs for younger members:

* Terms and Conditions apply. Premiums quoted are risk profile dependent and reviewed annually based on risk profile and economic factors.

“Unlike other Gap Cover providers products, GapX doesn’t group together all members into broad groups for individuals or families, pensioners or non-pensioners. Premiums are determined by the age of each person covered on the policy which prevents cross-subsidisation from young to old and from small families to larger families, ensuring the best possible premiums for younger individuals, younger and smaller families, as well as couples. All policies have one principal member and can add dependants to the policy where there is a relation, and all dependants must be on the same option as the principal,” explains Ceazare

To further build on the streamlining and efficiency momentum, GapX benefits and rules have been standardised and simplified, allowing for applications to be done via an online platform. “We realise that younger consumers are typically more tech savvy and comfortable doing their personal financial planning through digital platforms. The simplification and standardisation of the benefits make it a lot easier for consumers to understand and unpack what they are getting, and the application can be done fully online. GapX is exclusively a direct-to-consumer product.

“As South Africa emerges from the Covid-19 lockdown and experience the full impact of our economic situation, we can expect that consumers will be under tremendous financial pressure. Private healthcare will remain as important as ever in a post-Covid economy where public healthcare facilities will be stretched to and beyond breaking point. Finding ways to manage the costs of private healthcare will be crucial, and younger consumers need to look at appropriate health insurance solutions that are matched to the real risks they present, and that will see them through the financial impact of a potential health crisis,” concludes Ceazare.

For more information go to www.gapx.co.za

T’s and C’s apply. GapX is a product of GENRIC Insurance Company Limited (FSP 43638), an authorised Financial Services Provider and registered Short-term insurer.