African companies could free up an additional 33.5 billion dollars of working capital

If suppliers were to offer African companies payment terms of 30 days after delivery of goods and services, rather than demand payment in cash in advance, this could release more than USD 33.5bn of additional working capital to be put to more productive use in 2018, according to Euler Hermes.

In 2015, Euler Hermes estimated that if a payment term of 30 days were to be granted on the share of imports paid in cash (cash in advance), then it would free up over USD 40bn of working capital for African companies.

Since then, the trade picture has changed; a commodity shock hit resource-rich African countries and slashed their exports revenues, reducing further their capacity to finance imports even further. This contributed to the -22% fall in African import values from USD 800bn in 2014 to USD 623bn in 2016.

“Taking into account the new trade picture, our estimate stands at USD 33.5bn of working capital freed up for African companies in 2018. Lower imports combined with lower payment terms (64% of imports are paid in advance) explains this result,” Euler Hermes Chief Economist Ludovic Subran said.

Euler Hermes expects imports to grow at a +8% annual rate in this region. Should suppliers lengthen their payment term by 30 days, this would free about USD 45bn by 2020. The parallel development of trade finance is key to seize this great opportunity for the African continent.

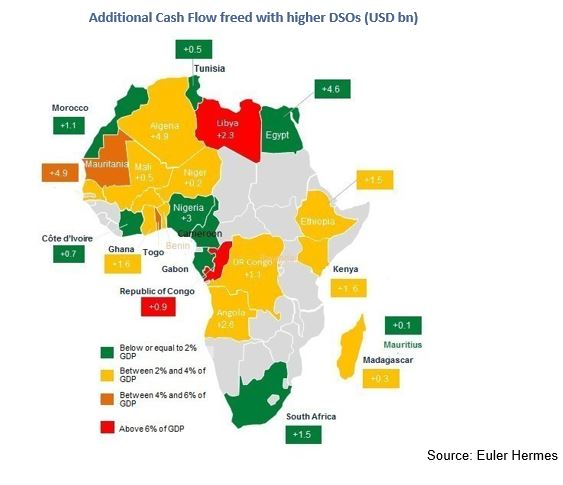

This huge amount of money wasted each year is a clear argument to develop domestic production capacity, since imports come with a cost due to low DSO[1]. Here are a few examples (chart below):

- Oil exporters (Algeria, Nigeria, Angola, Libya…) account for USD 14bn wasted in cash vaults as a result of short DSOs, with Algeria (USD 5bn, 3% of GDP) at the top of this ranking. The Republic of Congo, for instance, would free up the equivalent of 11% of its GDP (USD 0.9bn) with longer DSOs.

- In fast-growing East African economies, greater DSOs would also be a non-negligible growth boost. In Kenya for instance, it would free USD 1.6bn (2% of GDP), and about the same amount in Ethiopia.

- Potential gains are weaker in value in West Africa (USD 0.4bn in Senegal, 0.7bn in Côte d’Ivoire) but range from 2 to 2.5% of GDP. On the contrary, it means that these gains are lower in relative terms in countries with the highest income level: South Africa (0.4% of GDP), Morocco (1% of GDP).

The world is suffering from too long DSO in many places, but African figures show some divergence.

Stéphane Colliac, senior economist for Africa at Euler Hermes, said: “Big players are often bad payers, when small players have no opportunity to pay late. It is especially true in Africa: there is a paradox when we see that key State Owned Enterprises are able to postpone their payments by several years (e.g. in Angola or in the past in Egypt) while others have no other choice than cash payment. As an example, Moroccan main corporates have 84 days of DSO but 30% of the transactions (those involving smaller ones) are still paid in cash.”

[1] Days Sales Outstanding (DSO) is a measure of the average number of days that it takes a company to collect payment after a sale has been made. DSO can be calculated by dividing the number of accounts receivable during a given period by the total value of credit sales during the same period, and multiplying the result by the number of days in the period measured.