naamsa releases December 2022 new vehicle stats

Monday, January 09, 2023: NOTE TO THE MEDIA – naamsa says that despite multiple national and international headwinds, the South African motor industry’s recovery to pre-pandemic levels continued in 2022, albeit at a slower pace than 2021.

1. BRIEF COMMENT ON DECEMBER 2022 SALES

The new vehicle market registered its twelfth consecutive month of year-on-year growth during December 2022, with aggregate industry new vehicle sales at 41,783 units recording an increase of 5,839 vehicles or a gain of 16,2% compared to the total new vehicle sales of 35,944 units during the corresponding month of December 2021. The December 2022 new passenger car market and light commercial vehicle market reflected a sound performance with a year-on-year volume increase of 15,4% in the case of new passenger cars and a gain of 16,1% in the case of light commercial vehicles. Sales of medium commercial vehicles increased year-on-year by 36,9% while heavy commercial vehicles and buses increased by 23,1%.

Export sales in December 2022 ended the year on a positive note and at 26,302 units reflected a gain of 5,130 vehicles or an increase of 24,2% compared to the 21,172 vehicles exported during December 2021.

Overall, out of the total reported industry sales of 41,783 vehicles, an estimated 37,479 units or 89,7% represented dealer sales, an estimated 7,3% represented sales to the vehicle rental industry, 1,5% to government, and 1,5% to industry corporate fleets.

2. COMMENT ON 2022 NEW VEHICLE SALES AND VEHICLE EXPORTS: A YEAR CHARACTERISED BY MULTIPLE NATIONAL AND INTERNATIONAL HEADWINDS

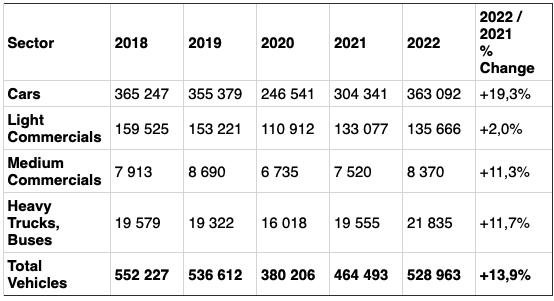

Following a robust recovery in the 2021 domestic new vehicle market, increasing year-on-year by 22,2% to 464,493 units compared to the severely COVID-19 affected 380,206 units in 2020, aggregate new vehicle sales recovered further by 13,9% to 528,963 units in 2022, but still 1,4% below the pre-pandemic 536,612 units sold in 2019.

New vehicle sales are regarded as a good barometer of the health of the domestic economy. Following a fairly upbeat first quarter 2022 industry performance, global supply chain disruptions along with the impact of the devastating floods in KwaZulu-Natal, elevated inflation, an upward trend in interest rates, record fuel prices, as well as record highs in the frequency and intensity of load shedding weighed heavily on both business and consumer confidence. However, the new vehicle market’s performance in 2022 remained resilient despite the the multiple national and international headwinds.

On a positive note, the lifting of all COVID-19 lockdown restrictions in the country in 2022 along with the recovery in business and leisure travel provided some support to the new vehicle market to counter the growing pressures on household incomes. However, the consumer trend of buying less expensive and smaller cars, usually SUVs or crossovers, continued in 2022. Stronger sales in the various commercial vehicle segments indicated improved business confidence, even in the tough economic times.

The following table summarises annual aggregate industry sales by sector since 2018 –

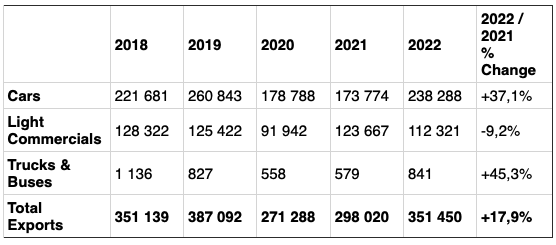

Although the KwaZulu-Natal flooding disaster left its mark on the industry’s performance and the country’s major logistics network during the year, vehicle exports at 351,450 units in 2022 reflected an increase of 53, 430 vehicles or a gain of 17,9% compared to the 298,020 vehicles exported in 2021.

The following table reflects the industry’s export sales performance since 2018 –

Global economic conditions have deteriorated significantly given persistently high inflation and aggressive interest rate hikes in many advanced and developing countries. The risks to export sales therefore reside on the downside for 2023, but growth prospects for domestic vehicle exports remain optimistic on the back of several new model introductions by major vehicle exporters.

3. INDUSTRY PROSPECTS FOR 2023: RETURN TO PRE-PANDEMIC LEVELS IN NEW VEHICLE SALES, VEHICLE EXPORTS AND DOMESTIC PRODUCTION AMIDST LOWER GLOBAL AND DOMESTIC GDP GROWTH

Just as COVID-19 pandemic-induced disruptions seemed to subside in 2022, Russia’s invasion of Ukraine has dealt a further blow to business and consumer confidence globally and in South Africa. The geopolitical conflict in Ukraine resulted in further supply chain disruptions and have inflated prices and the availability of strategic products and inputs. Energy prices have been at the centre of the inflationary surge and inflationary pressure, which caused an accelerated increase in interest rates in major world markets.

In South Africa, consumer price inflation reached a 13-year high, increasing to 7,8% in July 2022. As expected, the South African Reserve Bank in 2022 raised the interest rate for seven consecutive times since November 2021 and to its highest level since 2016. The higher stages of load-shedding also seemed to have an amplified negative impact on production and the South African economy as a whole. However, despite the myriad of negative economic pressures and ongoing stock supply shortages, the new vehicle market continued to outperform expectations in 2022.

As far as 2023 is concerned, the domestic new vehicle market’s performance is expected to remain resilient despite weakening domestic economic indicators and a deteriorating global growth outlook. Growing concerns about global “stagflation”, which is high interest rates combined with slow growth and high inflation, the continued economic impact and disruption of supply chains resulting from the Russia-Ukraine war, and the current pace of tighter monetary policy in major markets have increased the possibility of a global recession. There is also a likelihood of further near-term global supply chain disruptions stemming from the rapid re-opening of the Chinese economy that has resulted in surging COVID-19 infections.

GDP growth in South Africa continues to be adjusted downwards and was now expected to be at 1,1% for 2023. In view of the close correlation between new vehicle sales and the country’s GDP growth rate, single digit growth in new vehicle sales could be expected for 2023 as the market returns to pre-pandemic levels in sales and exports.

A key priority focus for the South African government in 2023 is to finalise the support framework for NEVs, considering the importance of timing of the interventions so that they were aligned with investment decisions and lead times of the OEMs when considering next-generation models.

Best wishes for 2023 to the media and all automotive industry stakeholders.